How Down Payments Affect Loan Terms

Your down payment plays a major role in how a loan is structured. It doesn’t just affect how much you borrow—it can change your interest rate, monthly payment, and even whether you qualify for certain loan programs.

What is a down payment?

A down payment is the amount you pay upfront when purchasing something like a home or car. The rest is financed through a loan.

Example:

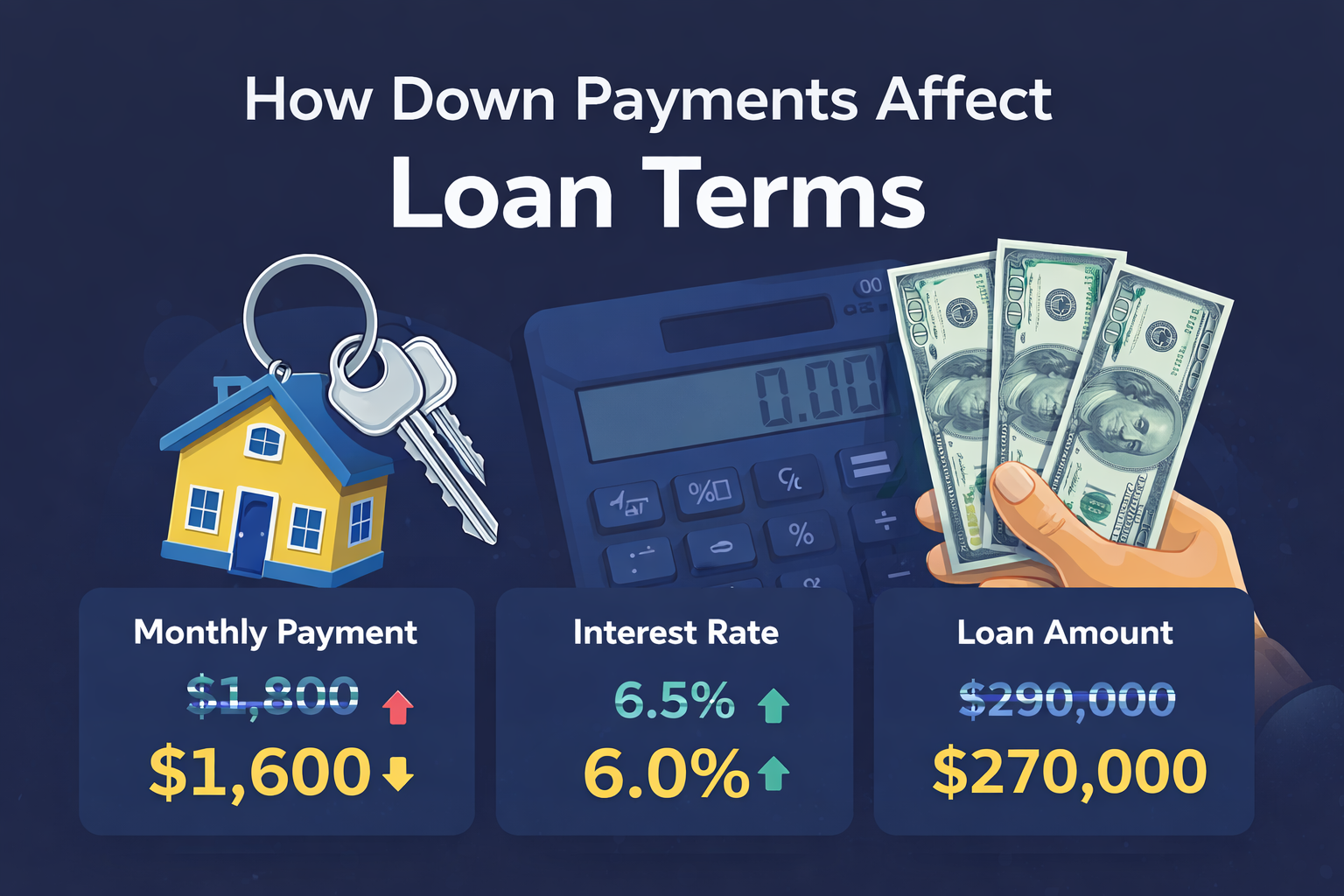

- Home price: $300,000

- Down payment (10%): $30,000

- Loan amount: $270,000

How down payment affects your loan

1. Loan amount

A larger down payment reduces how much you need to borrow. This directly lowers your monthly payment and total interest paid over time.

2. Interest rate

Lenders often offer better interest rates to borrowers who put more money down. A larger down payment lowers the lender’s risk.

3. Monthly payment

Since you’re borrowing less, your monthly payment is lower. This can also improve your chances of approval.

4. Loan requirements

Some loan programs require minimum down payments, while others allow very low or even zero down depending on eligibility.

5. Mortgage insurance (important)

If your down payment is less than 20% on a home, you may have to pay for mortgage insurance. This increases your monthly payment.

How this impacts approval

A higher down payment can improve your approval chances because it reduces the lender’s risk and lowers your monthly payment.

Since your monthly payment is a key part of your debt-to-income ratio, putting more money down can help you qualify more easily. If you want to understand how lenders evaluate that, read What Is a Good Debt-to-Income Ratio? .

Is a bigger down payment always better?

Not always. While a larger down payment lowers your loan costs, it also means tying up more cash upfront.

- Lower down payment = more cash on hand

- Higher down payment = lower long-term cost

The right choice depends on your financial situation and goals.

Simple takeaway

- Higher down payments reduce loan size and monthly payments.

- They can improve interest rates and approval chances.

- Lower down payments increase cost but require less upfront cash.

See what you may qualify for based on your down payment and income.