What Debt-to-Income Ratio Do Lenders Actually Use?

When applying for a loan, you may hear about different types of debt-to-income ratio (DTI). But which one do lenders actually use when making a decision?

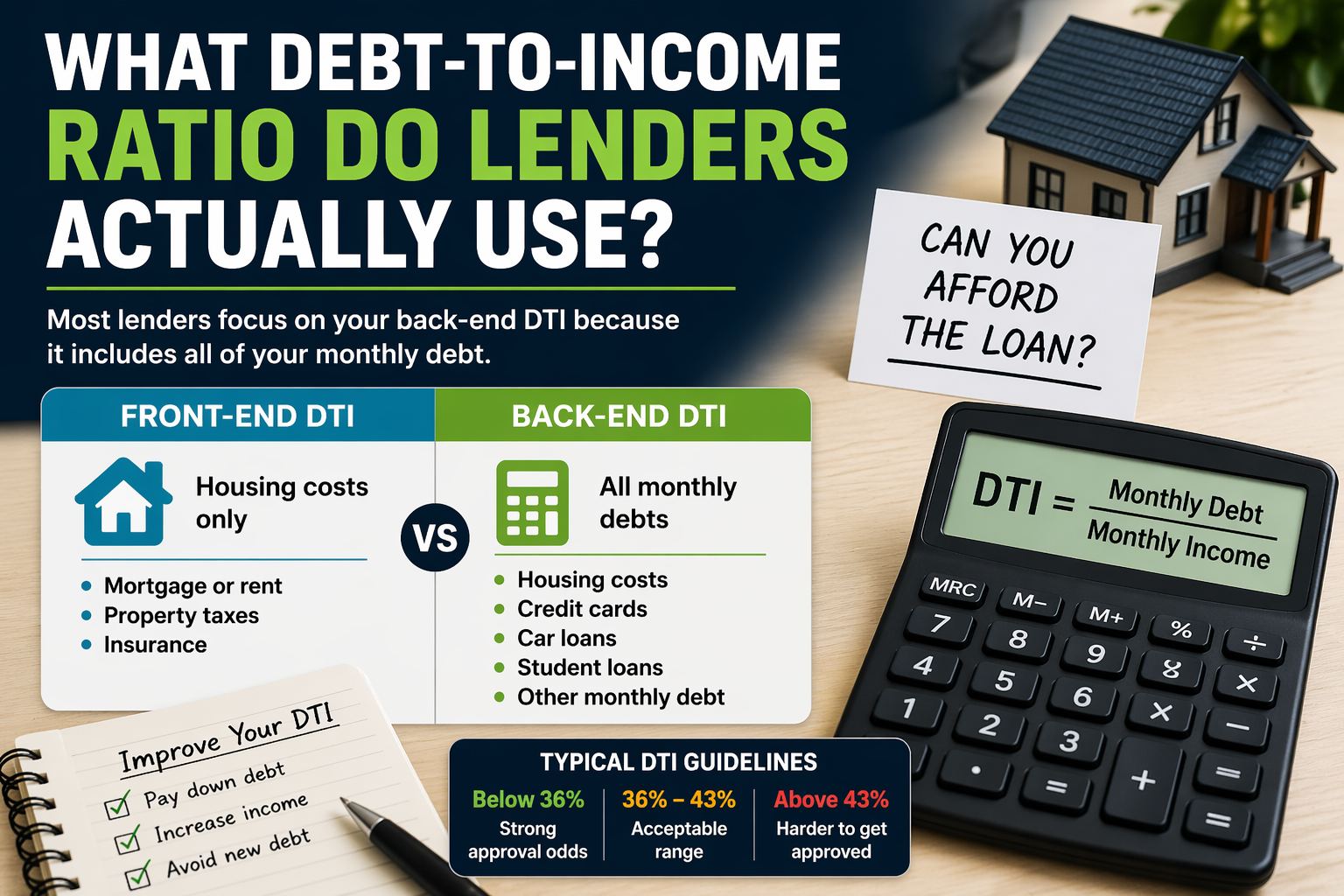

Quick answer

Most lenders focus on your back-end DTI because it includes all of your monthly debt and gives the most complete picture of your finances.

What lenders are really looking at

Lenders want to know one thing: can you afford the loan? Your DTI helps answer that by comparing your monthly debt to your income.

Front-end vs back-end DTI

There are two types of DTI:

- Front-end DTI → housing costs only

- Back-end DTI → all monthly debts

If you want a full breakdown of the difference, see What Is Front-End vs Back-End DTI? .

Why back-end DTI matters more

Back-end DTI includes everything you owe each month. This gives lenders a clearer view of your total financial obligations.

- Credit cards

- Car loans

- Student loans

- Housing costs

Typical DTI limits

Most lenders prefer:

- Below 36% → strong approval odds

- 36%–43% → acceptable range

- Above 43% → harder to get approved

For a deeper look at what’s considered good, read What Is a Good Debt-to-Income Ratio? .

How to improve your DTI

- Pay down existing debt

- Increase your income

- Avoid taking on new loans before applying

Simple takeaway

- Lenders mainly use back-end DTI

- Lower DTI improves approval chances

- Your full debt picture matters more than just housing

See how new debt affects your overall DTI.

Your credit score and DTI both impact loan approval.